If you’re self-employed or running a small business, this question usually pops up at the worst possible moment.

Often late at night.

Usually after a good month.

Sometimes followed by a quiet sense of panic.

“How much of this is actually mine?”

“How much should I not touch?”

“What if I get this wrong?”

Let’s clear this up properly.

Why this question causes so much stress

Most people don’t struggle because tax is complicated.

They struggle because nobody gives them a straight answer.

You hear things like:

-

“Put aside 20%”

-

“No, make it 30%”

-

“I just wait until the bill comes”

-

“HMRC will tell you”

None of that builds confidence.

What you actually want is a simple, realistic rule that keeps you safe without ruining your cash flow.

First, the uncomfortable truth

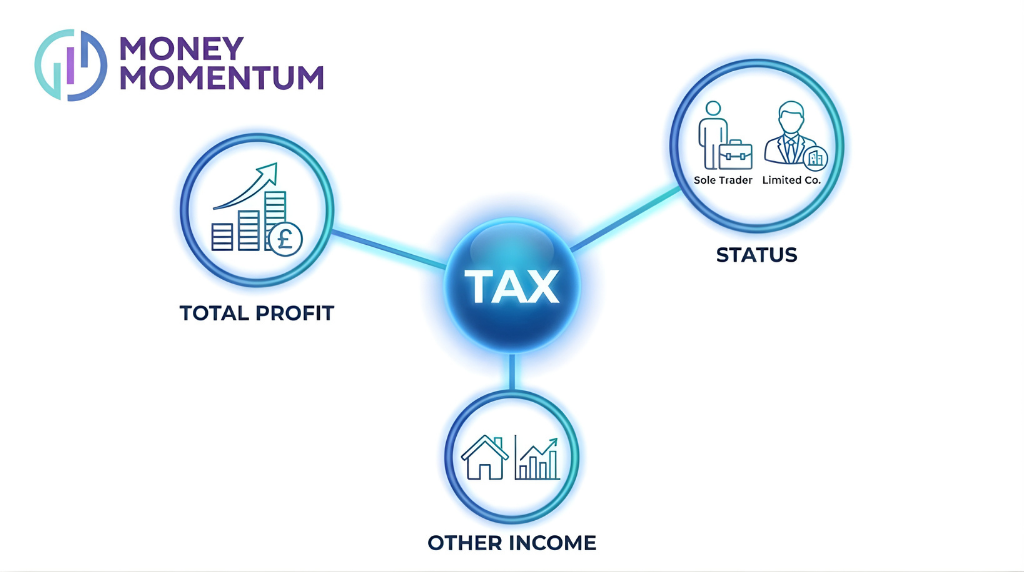

There is no single magic percentage that works for everyone.

Your tax depends on:

-

Your total profit

-

Whether you’re a sole trader or limited company

-

Other income you have

-

Personal circumstances

But that doesn’t mean you have to guess.

It just means you need a sensible working approach, not a perfect calculation every month.

A simple starting point that works for most people

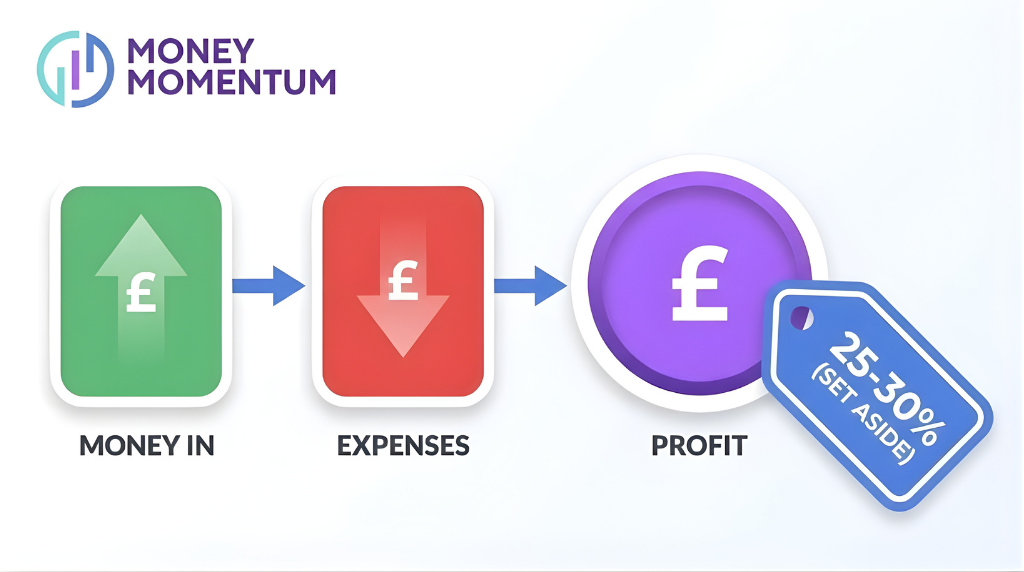

For most UK sole traders and self-employed people, a safe monthly rule of thumb is:

👉 Put aside 25–30% of your profit

Not turnover.

Profit.

That means:

Money in

Minus business expenses

Equals the number you base this on

This won’t be exact to the pound, but it keeps you out of trouble.

Why profit matters more than turnover

This is where many people trip up.

If you earn £5,000 in a month but spend £2,000 running the business, you’re not taxed on £5,000.

You’re taxed on £3,000.

Putting money aside from turnover usually feels painful and unnecessary.

Putting money aside from profit feels fair and manageable.

What if 30% feels like too much?

That’s a real concern, especially in the early stages.

If cash is tight, the worst thing you can do is pretend tax doesn’t exist.

A better approach:

-

Start at 20%

-

Review it every few months

-

Increase it as income stabilises

Consistency matters more than perfection.

Zero planning is what causes panic later.

Limited company? Slightly different picture

If you run a limited company, tax planning works differently.

You’re dealing with:

-

Corporation Tax in the company

-

Personal tax when you take money out

-

Timing differences

In simple terms:

-

The company should set aside money for Corporation Tax

-

You personally should plan for tax on salary or dividends

This is where having clarity really pays off, because guessing here can get expensive.

The biggest mistake people make

Waiting until the tax bill arrives.

At that point:

-

The money is already spent

-

The stress is high

-

Decisions feel rushed

Tax shouldn’t be a surprise.

It should feel expected.

When people tell us “the tax bill wasn’t as bad as I feared”, it’s usually because they planned monthly.

A practical habit that makes this easy

One simple habit helps massively.

Open a separate savings account.

Label it “Tax”.

Move the money monthly.

Out of sight really does help here.

It turns tax from a looming threat into a boring admin task. And boring is good.

Final thought

You don’t need to be exact every month.

You just need to be intentional.

Putting money aside regularly gives you control, confidence and calm.

And when tax time comes around, it stops being scary.

It just becomes another line item you already planned for.